How to Budget Your Money and Save

According to the NBER, 75% of American households would not be able to come up with $2,000 dollars if given 30 days.

Are you a part of the 25% who could come up with the money, or are you a part of the 75%?

Is there too much month left and not enough money? It’s time to learn how to budget. In this article, we’re going to make sure that you’re part of the 25% by covering:

- How budgeting fits in your life

- Tools you need, including a few free options

- The 4 steps to effective budgeting

- Awesome tips to save even more money

- What to do with your saved money

Let’s get started!

How Does a Budget Fit In With Your Life?

Running a home and raising a family keeps you busy, I get that. It gets even harder when you don’t have enough money at the end of the month. I know budgeting sounds like another chore to add to your already long list of things to do…

But what if?

What if I told you that budgeting could help relieve money pressures from your life?

Are many of your stresses financial based? I know when I was a kid, my parents always fought about money.

Creating a budget doesn’t have to be another stress in your life. Think of it as a medicine for your financial stress. It doesn’t fix all of your problems right away, and it doesn’t taste good, but if you keep taking it, you’ll start to feel better.

Creating a budget takes a little time up-front, but once it’s made, you just need to tweak it as time goes on. Just remember: you have to be willing to do whatever it takes, even if it means giving up things you like, and choose to change your lifestyle to make it fit within your means.

You can do it, and I’m going to help you.

Tools You Need For Budgeting

- Pencil

- Paper

- Calculator

- Or a spreadsheet program like Microsoft Excel, Google Sheets (free) or Openoffice Calc (free)

Writing everything down with pencil and paper is an excellent way to plan your budget, especially if you’re not comfortable with spreadsheets. You can always correct things written in pencil and get yourself some different versions of your budget to see what version suits you best.

You should break out your calculator as well. There will be some calculating going on and you want to have an accurate count. Calculators can save you from having to live with mistakes.

Budgeting Apps and Software

If the pencil and paper route are not what you like, there are also budgeting applications available like Mint.com, where you can create your budget electronically. Check out our review of Mint vs. EveryDollar if you want to see a great feature comparison of two very popular budgeting applications.

Step 1: Budgeting Should Start With Goals

Goals help you laser-focus your plans. What do you hope to accomplish with your budget? Saving more money sounds nice, but what does “more money” mean? A better goal would be to save $1,200. But it’s not a great goal. What makes a great goal? A definite outcome and a time frame.

Here is an example of a great goal: to save $1,200 over the next year.

It is a clear, achievable goal with a deadline.

By setting specific goals, you can better understand what you need to do to reach them. What are some other types of goals you can set?

Eliminating Debt

Eliminating debt is a great goal. You might find that you’re a little over-extended in the credit card department and would like to get that under control. Or maybe you want to pay off your student loans. Those are both great outcomes for your goals.

Just Having Enough Money

Maybe you just want to eliminate the whole experience of not having enough at the end of the month, and your goal (and reward) would be no more stress at the end of each month. This is a wonderful and completely respectable reason to start budgeting.

Buying Things Without Credit Cards

Perhaps you want to teach yourself how to save for the things you want rather than putting everything on credit cards. This is a lesson that many people need to learn, but probably won’t. You’re different though, I can feel it!

Write Your Goals Down

Write down at least one goal that you would like to accomplish, along with the timeline you can realistically achieve it in. This will be what we use to help us setup the rest of the budget.

Step 2: Get Your Whole Financial Situation In Front of You

Now you need to gather up all your bills and receipts and lay them out on your table. You want things like receipts, earning statements, bank statements, and bills. After you lay them out you’ll want to separate them into 2 separate categories which are:

- Incoming

- Outgoing

Get yourself a total of both categories. You may find yourself getting a little nervous at this point, but don’t worry, you’ll find there are things in your budget you can do without that can help bring you into that ‘stress-free end of the month’ lifestyle you want.

It also helps to separate your bills (outgoing) from your pleasures (also outgoing). You can put the water bill, electric bill, and credit card receipts and the like, all together. Now you can make another pile from ‘dining out’ receipts, movie tickets, movie rentals, game rentals, etc.

NOTE: All of the things above are outgoing. Some are totally necessary and others can be changed or cut down so you have that extra money you’ve been needing at the end of each month.

Step 3: Create the Budget

Now that everything you need is right in front of you, it’s time to make decisions about what and where to cut. You need to cut out whatever it takes to meet your goal from step 1. There are two ways you can do it, the simple way or the detailed way.

The Simple Budget

The simple budget is a nice way to budget if you have a relatively minor goal to achieve. Basically, it involves controlling your spending in 1 area. For example, cooking food at home more often, or ordering from take-out restaurants rather than pricier dine-in restaurants.

Another common thing people do is give up a habit like buying their morning coffee. This is the easiest kind of budget you can do, simply cutting money in one area, but if you have bigger budget issues, such as spending more than you make and wanting to establish savings, then you probably need the detailed budget.

The Detailed Budget

Your other option is to categorize all of your income and expense items then figure out where to make cuts. First start by writing down your income and your actual spending. I like to break expenses into 3 categories:

- Fixed expenses: These are non-negotiable fixed amounts that you must pay each month.

- Variable expenses: These are expenses that fluctuate. Some of them you might be able to get rid of, but many you can’t.

- Optional expenses: These are expenses, either fixed or variable cost that you can eliminate if needed.

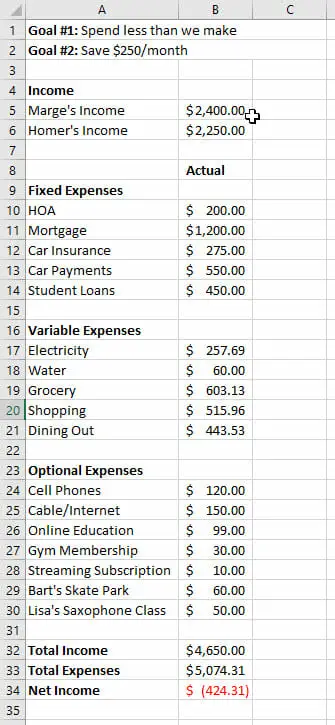

Here’s an example budget I made and included sample “actual spending” data in it:

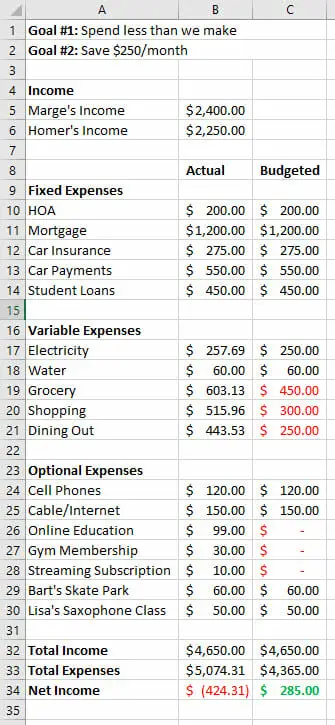

Next, create another column for “budgeted.” In this column, this is where you figure out where you can make cuts. Here’s my example. I put cuts in red to make them easier to find.

How Much Do I Have to Cut from My Budget?

The amount you have to cut will depend on what the goals were in step 1. In my example, this couple put their goals at the top of the spreadsheet. Not only do they spend more than they make, but they also want to save $250 dollars each month. That means, they’ll need to cut out nearly $700 dollars per month from their budget!

In my example above, we decided to cut our grocery shopping by using coupons and doing a lot more shopping at a discount grocery store. We also decided to cap our frivolous shopping to only $300 each month and dining out to $250 each month. On top of those cuts, we canceled our online education subscription, our gym membership (we weren’t using it anyways) and our streaming subscription.

If you need help with ideas for cutting costs, here are two examples:

Grocery Store Savings Example

For example, groceries are the classic variable cost budgeting item. How much have you been spending on groceries? If you typically spend $500 each month on groceries, can you reduce it to $400?

How do you reduce your grocery spending that much? Coupons are the first and most obvious step. If that doesn’t do it, then consider switching grocery stores. My family now does nearly all of our shopping at a discount grocery chain called Aldi. It routinely saves us hundreds each month. Consider getting rid of brand loyalties, only buy items when they’re on sale and stop buying pre-made foods. All of these tips will help you shave money from the grocery bill.

Cutting Cable TV

My family has been without cable television for over 5 years now. Lots of people wonder how we’re able to live like this. When we watch TV, we wonder how people can pay money for it. The sheer number of commercials alone is distracting. We thought we were making a sacrifice, but actually ended up preferring life without regular TV. We have Netflix and love it.

Other Budget Areas Where We Can Save Money

There were plenty of other spots that I could have cut. I wouldn’t hesitate to get rid of cable (although Internet would need to stick around). I also would switch phone carriers to something cheaper. We could probably save a little on electricity by adjusting the household temperature and making sure we’re not leaving lights and TVs on all day.

Other more drastic options would be selling the cars and buying a used, but paid for vehicle (this would also drop the car insurance down). Lastly, sometimes life requires everyone to make sacrifices, so the kid’s sax class and the other kid’s skate park memberships might need to be cancelled.

Step 4: Control Your Spending and Stick to the Budget

One of the hardest things about creating a budget is sticking to it once it’s created. It’s tougher at first until you get used to doing without some things that sort of made your life feel worth living.

However, when the end-of-the-month headaches disappear you can feel a sense of pride in taking responsibility for your budget and household. And who knows, maybe you won’t miss the things you think you need. That’s how we felt about cable. So, how do you stick to your budget?

You can use a free app like Mint.com to help keep track of your spending or other tools like You Need a Budget. You can keep your budget with you so you’re always reminded. Another option is to kick it old school and use the envelope budgeting method.

Another great tip is to ditch the credit and debit cards. Switch to cash so you always know how much you have available to use and can’t spend more than you have. It seems scary at first, but don’t worry, most of your fears won’t come true.

What Do I Do with the Money I’ve Saved with my Budget?

Once you get to this point, it can be hard to remember where you started. Remember what we did at the very beginning of this guide? We established our goals. Naturally, what you do with the money saved from budgeting should be used towards the goals you set!

Eliminate Your Debts

One of the main goals for many families is to get out from under the constant credit card payments. If you want to reduce your credit card debt, work on one card at a time. Start with the highest interest card and work your way through them.

Find money within the cuts you’ve made in your lifestyle, to make a larger than minimum payment on one card every month, while maintaining the minimum on the others. Once that card is paid off you will have saved on interest by paying more than the minimum, and now you can start on the next card with the money you were using to pay off the first card.

Create an Emergency Fund

Consider setting some of the savings aside as an emergency savings fund and use the remainder to pay down other debts. Once you’re debt free, you can then just pile the money up sky high, invest it or save for retirement. Honestly, once you’ve taken this much control of your finances, you really can do almost anything.

How to Budget Wrap Up

Budgeting is all about knowing what you have coming in and what you have going out. Sometimes it becomes very easy to lose track of how much is going out and we spend without caution. That’s how people wind up in such dire straits financially.

If you and your family are in need of a budget just follow the steps laid out above. If you want to get online and do it then go to Mint.com and get signed up, it’s free and I use it. Having a realistic budget will make things easier on everyone over the long haul. Give stress a rest and save yourself some headaches by learning how to budget and staying within your budget.