In early 2019, I left my traditional job and needed to roll my 401(k)s over. Yes, I had multiple. I had a traditional 401(k) and a Roth 401(k). Since 2017, I’ve been using Betterment as my primary investment broker.

I have accounts with Schwab, Robinhood, and Ally Invest as well, but I like how easy and hands-free Betterment is. Read my Betterment review if you want to learn more. I chose Betterment over Wealthfront, but I use Robinhood often too. Read my Robinhood vs Wealthfront faceoff if you’ve considered those options as well.

Betterment has an easy-to-use interface, and Betterment’s pricing is very reasonable for the features they offer. So, I decided that Betterment would become the new home for my 401(k)s- well, technically IRAs. Thus, my adventure into 401(k) rollovers began.

Before we get into this, I do want to mention that this is all from my personal experience. I’m not a CPA, a tax expert, a financial planner, nor do I have any of the necessary licenses to provide you with formal financial advice. I’m just letting you know what my personal experience was, and you should consult with your financial advisors before making any big changes to your finances. There can be significant tax consequences if you do things incorrectly.

I had a Roth 401(k) and a Traditional 401(k) to Rollover, so How Did It Go?

In short, it went well. Even though mine was a bit more complicated than average, I was impressed with how well it was all managed. Read further to learn more about the details of a 401(k) rollover, and what you can expect. If you have more general questions about 401(k) rollovers, then make sure you read “401k Rollovers: Can I Rollover a 401k to an IRA?” It answers lots of general 401k rollover questions.

What to Expect When Rolling Over Your 401(k)

You likely have a traditional 401(k) or a Roth 401(k). If your 401(k) is with a large provider like Fidelity or Vanguard, then your process will likely be very seamless. Those types of rollovers are called “synced” or “expedited” rollovers.

If you’re with a smaller provider or you have a more complicated transfer (such as my two different kinds of 401(k)s), then you go through an “unsynced” rollover, which is a more manual process that involves people and mailing checks. It’s not a bad process, just a bit slower. We’ll cover all of that as we go through this review.

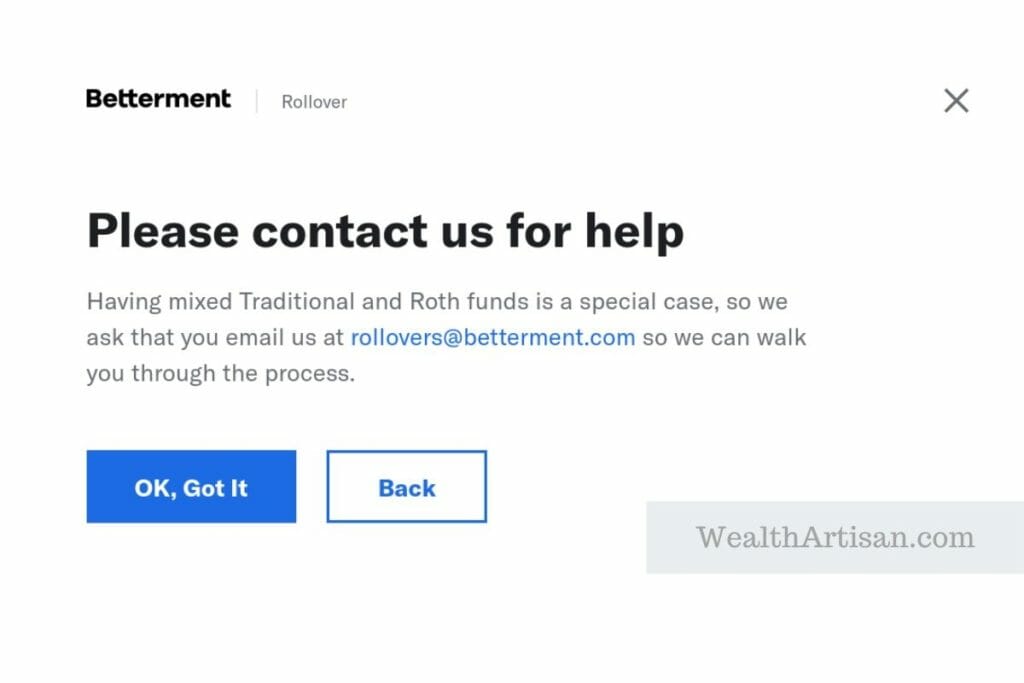

What is a Mixed 401(k) Rollover?

A mixed 401(k) rollover is precisely what my rollover was. It’s when you’ve got multiple types of 401(k)s. When I attempted to initiate my rollover online, this was the message I received:

If you’re unsure about which kind of 401(k) you have, then log into your 401(k) providers website, locate the name of your account, and it should have the account type in the title.

Often, you’ll see the words “traditional” or, more rarely, “Roth.” If you see two different accounts, then you may have a mixed rollover. You can also contact your plan administrator’s customer support to find out what kind of 401(k) you have. If you have only one account in your 401(k) plan, then chances are your rollover will be smooth.

Roth 401(k)s are relatively uncommon, partly because they are a newer offering compared to the traditional. Roth 401(k)s didn’t exist until 2006, whereas Congress created the traditional 401(k) in 1978.

Starting a 401(k) Rollover

Getting started is as simple as logging into your Betterment account and selecting the “Deposits and Rollovers” option, then clicking on “401(k) Rollover.” Once you’ve done that, you’ll be taken through a short questionnaire to determine how your rollover will proceed.

As of this writing, this is the current list of “synced” or “expedited” 401(k) rollover providers.

Betterment Expedited 401(k) Providers:

If your provider isn’t on the list, then you’ll likely have to go through the “unsynced” process. That sounds like a bad thing, but it’s not. I went through the “unsynced” method, and it was smooth.

The Expedited Rollover Process

My “mixed” rollover was a bit more involved. I didn’t go through the expedited process, but I contacted Betterment customer support to learn more about what this process involves and how long it takes.

They said that, by following the prompts inside Betterment, you’d automatically have the correct kind of IRA opened in your account, and they’ll email you personalized instructions on the exact next steps you need to take with your plan administrator.

I did have questions about the “expedited” turnaround time, and this was their response:

“The timeline for doing the transfer depends on how long it takes the current provider to process the request, liquidate the account, and send us a check. It also varies a lot whether or not the provider will charge a fee and how much the fee will be, but Betterment does not charge any fees for transferring in.”

That’s an honest answer. If I had to guess the fastest turnaround possible, using my experience as an example, then I could see everything being complete in 5-7 days. That’s assuming everything goes perfectly, and your administrator overnight mails the checks. Remember, your current plan administrator needs to liquidate your account before transferring, so there will always be some wait time.

The Unsynced Rollover Process

The process I went through was the “unsynced” process. You contact [email protected] to get things started. They provide you with instructions to deliver to your plan administrator.

I had to create both a traditional IRA and a Roth IRA inside a Betterment “Retirement” goal to get things started. That’s because I had a Traditional and a Roth 401(k). If you only have a traditional 401(k), then you’ll only need to create a traditional IRA. Don’t worry, though; they’ll tell you exactly what you need to do.

Once I created the accounts, they sent me all of the information that my plan administrator would need to write the checks correctly. Overall, it took two weeks to complete from my initial email, but part of that wait was because I was asking a lot of questions. Overall, it probably could have been done in about 7-10 days.

Essentially, your plan administrator will mail a check to Betterment to perform what is called a “direct rollover.” Your plan administrator must fill out the check a specific way, so Betterment knows which account to credit. My plan administrator was a little awkward and refused to send the checks directly to Betterment because they weren’t on the “direct rollover list,” so they made the checks out to Betterment, then sent them to me to forward.

Betterment 401(k) Rollover Wrap-up

I hope my experience in rolling over a 401(k) helps you in some way. In a way, it’s pretty neat that I had one of the more complicated types of rollovers because it makes me all the more confident in reassuring all of my readers that their rollover will go smoothly. If you want to read more about Betterment 401(k) rollovers, then check out this article from Betterment.

Questions You Might Have:

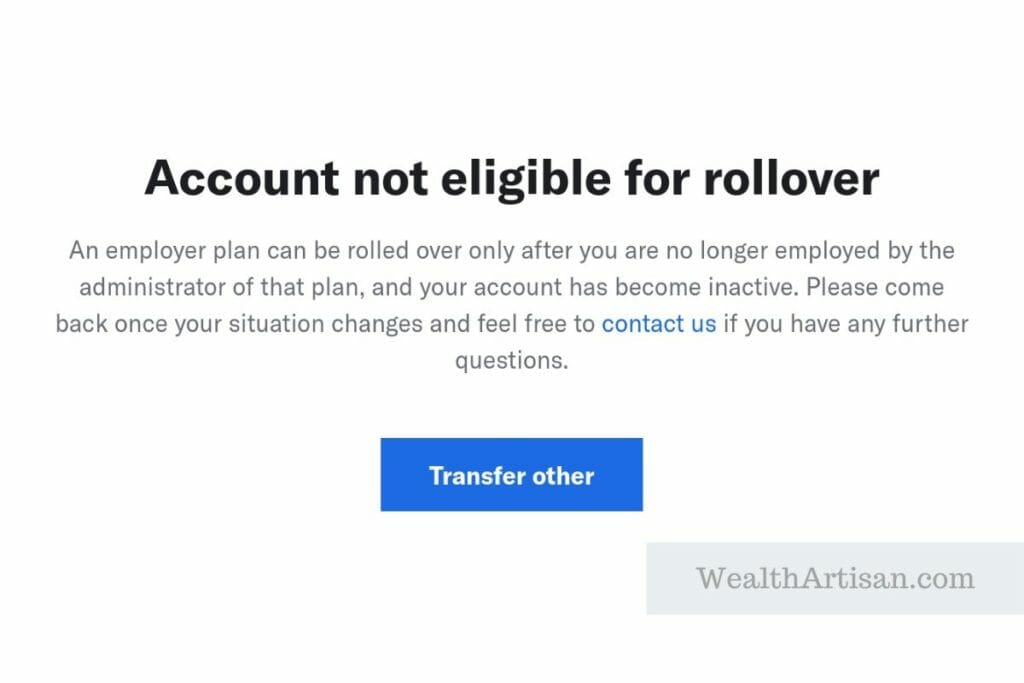

Can I Transfer my 401(k) to Betterment?

Yes, you can. It must be an inactive 401(k), meaning you no longer work for your employer. The 401(k) will be rolled over into an IRA of the same type (traditional, or Roth).

Are There Fees for Rolling Over a 401(k)?

Betterment does not charge fees for rolling a 401(k) over to them. Most providers wouldn’t because you’re moving assets to them, and they’re going to make money from it. However, your current plan administrator may charge a fee for the rollover. Betterment does have its fees for asset management and advisory services. Make sure you check out our Betterment pricing review.

Can I Roll an Active 401(k) Over to Betterment?

No, at this time, Betterment requires that you no longer be employed by the plan administrator to perform a rollover.

Can I Rollover a 401(k) That Has an Active Loan?

It may vary based on your plan administrator, but my plan administrator allowed the following options with my outstanding 401(k) loan:

- Pay the loan back in full, then do the rollover.

- Closeout the loan as a distribution, which will create a taxable distribution, then perform the rollover.